Popular on TelAve

- Althea Gibson Honored as Final Release in U.S. Mint's American Women Quarters Program - 155

- Cyntexa Announces Updates to ChargeOn on Salesforce AppExchange

- TradingHabits.com Launches to Support Day Trader Well-being

- 5,000 Australians Call for Clarity: NaturismRE's Petition Reaches Major Milestone

- BumblebeeSmart Introduces Rounded Busy Board Set for Preschoolers

- Americans Are Trading Offices for Beaches: How Business Ownership Enables the Ultimate Location Freedom

- Wohler announces three SRT monitoring enhancements for its iVAM2-MPEG monitor and the addition of front panel PID selection of A/V/subtitle streams

- Dental Care Solutions Unveils New Website for Enhanced Patient Engagement

- WHES Retains BloombergNEF Tier 1 Ranking for Sixth Consecutive Quarter

- Huntington Learning Center of Russellville Marks 1 Year Anniversary; Extends Reduced Grant-Aligned Rates to All Students in Learning Center Services

Similar on TelAve

- Verb™ Presents Features Vanguard Personalized Indexing: Utilizing Advanced Tax-Loss Harvesting Technology

- UK Financial Ltd Announces A Special Board Meeting Today At 4PM: Orders MCAT Lock on CATEX, Adopts ERC-3643 Standard, & Cancels $0.20 MCOIN for $1

- From Cheer to Courtroom: The Hidden Legal Risks in Your Holiday Eggnog

- Record Revenues, Debt-Free Momentum & Shareholder Dividend Ignite Investor Attention Ahead of 2026–2027 Growth Targets: IQSTEL (N A S D A Q: IQST)

- $80M+ Backlog as Florida Statewide Contract, Federal Wins, and Strategic Alliance Fuel Next Phase of AI-Driven Cybersecurity Growth: Cycurion $CYCU

- High-Conviction CNS Disruptor Aiming to Transform Suicidal Depression, Ketamine Therapeutics, and TMS - Reaching Millions by 2030

- Talagat Business Academy Announces Joint Certificate Program With The University of Chicago Booth School of Business

- Slotozilla Launches New Report on How AI Is Reshaping Careers and Society

- Explosive Growth in U.S. Cryptocurrency Cloud Mining Sets The Stage for New Platform Launch with Daily Rewards in a Transparent Revenue-Share Model

- Qtex Cierra Ronda de $7 Millones para Estandarizar la Banca Transfronteriza en los Mercados Emergentes de Latinoamérica

First Bancorp of Indiana, Inc. Announces Financial Results September 2025

TelAve News/10880471

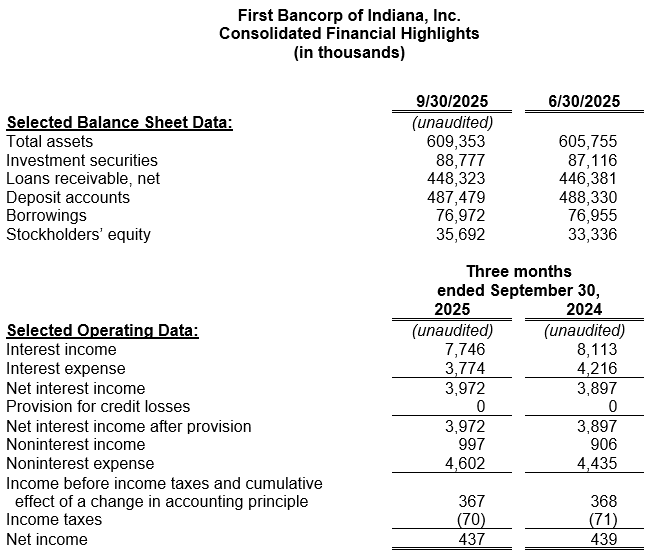

EVANSVILLE, Ind. - TelAve -- First Bancorp of Indiana, Inc. (OTCPK:FBPI), the holding company (the "Company") for First Federal Savings Bank (the "Bank"), reported earnings of $437,000 ($0.26 per diluted common share) for the first fiscal quarter ended September 30, 2025, compared to $439,000 ($0.26 per diluted common share) for the same quarter a year ago. Earnings for the three-month period equate to a return on average assets ("ROAA") of 0.29% and a return on average equity ("ROAE") of 5.21%. This compares to an annualized ROAA of 0.28% and an annualized ROAE of 5.40% last fiscal year.

Net interest income for the quarter ended September 30, 2025, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.86% for the quarter ended September 30, 2025, an improvement from 2.67% as reported for the quarter ended September 30, 2024. Gains on loan sales accelerated in the most recent quarter. The quarter over quarter rise in total non-interest expenses was largely attributed to increased compensation expense and to advertising costs from a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $88.8 million on September 30, 2025. No investments were added, so the modest increase was attributed to an improvement in the portfolio's fair market value.

Net loans outstanding, which totaled $448.3 million on September 30, 2025, have increased $1.9 million during the quarter. Commercial loan production increased to $14.1 million for the three-month period, which included one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, totaled $5.6 million during the same timeframe. Construction lending slowed during the quarter and accounted for 7.5% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $5.9 million.

No provision for credit losses on loans was recorded in the three months ended September 30, 2025 or 2024. Net loan chargeoffs totaled $32,700 for the quarter, compared to $75,800 for the comparative quarter last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.29% on September 30, 2025, compared to 1.60% a year ago, primarily as the result of the successful restructuring of two large commercial relationships. Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.28 million at September 30, 2025, compared to $5.58 million on September 30, 2024. The portion of the allowance attributed to the loan portfolio represented 1.13% of at-risk loans on September 30, 2025, compared to 1.11% last year. Although management believes that the allowance is adequate, a slowing economy and persistent inflation may have an adverse effect on the credit quality of the loan portfolio. Management remains in close contact with our most vulnerable borrowers and will make additional provisions to the allowance, as necessary.

More on TelAve News

Deposit accounts, totaling $487.5 million on September 30, 2025, declined by $851,000 since the beginning of the fiscal year. Growth in local deposits during the first fiscal quarter has allowed the Bank to retire $17.2 million of higher-costing wholesale funding. Conversely, local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.56% for the current quarter compared to 2.71% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.70% for the quarter, compared to 2.89% for the quarter ended September 30, 2024.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At September 30, 2025, First Federal Savings Bank maintained lines of credit totaling $15.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($12.6 million) and the Federal Home Loan Bank ($82.4 million).

Stockholders' equity totaled $35.7 million on September 30, 2025, which includes a $7.8 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized if a security is sold. The increase in stockholders' equity is primarily due to the Company's earnings and a decrease in the unrealized loss on the Bank's available for sale investment portfolio. Based on the 1,704,992 outstanding common shares on September 30, 2025, the book value per share of FBPI stock was $20.93, compared to $20.63 on September 30, 2024.

On September 30, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios were 8.92%, 12.79%, and 14.01%, respectively - improvements from 8.36%, 11.76% and 12.98% on September 30, 2024.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

More on TelAve News

Net interest income for the quarter ended September 30, 2025, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.86% for the quarter ended September 30, 2025, an improvement from 2.67% as reported for the quarter ended September 30, 2024. Gains on loan sales accelerated in the most recent quarter. The quarter over quarter rise in total non-interest expenses was largely attributed to increased compensation expense and to advertising costs from a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $88.8 million on September 30, 2025. No investments were added, so the modest increase was attributed to an improvement in the portfolio's fair market value.

Net loans outstanding, which totaled $448.3 million on September 30, 2025, have increased $1.9 million during the quarter. Commercial loan production increased to $14.1 million for the three-month period, which included one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, totaled $5.6 million during the same timeframe. Construction lending slowed during the quarter and accounted for 7.5% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $5.9 million.

No provision for credit losses on loans was recorded in the three months ended September 30, 2025 or 2024. Net loan chargeoffs totaled $32,700 for the quarter, compared to $75,800 for the comparative quarter last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.29% on September 30, 2025, compared to 1.60% a year ago, primarily as the result of the successful restructuring of two large commercial relationships. Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.28 million at September 30, 2025, compared to $5.58 million on September 30, 2024. The portion of the allowance attributed to the loan portfolio represented 1.13% of at-risk loans on September 30, 2025, compared to 1.11% last year. Although management believes that the allowance is adequate, a slowing economy and persistent inflation may have an adverse effect on the credit quality of the loan portfolio. Management remains in close contact with our most vulnerable borrowers and will make additional provisions to the allowance, as necessary.

More on TelAve News

- 6 Holiday Looks That Scream "Old Money" But Cost Less Than Your Christmas Tree

- From Cheer to Courtroom: The Hidden Legal Risks in Your Holiday Eggnog

- Controversial Vegan Turns Rapper Launches First Song, "Psychopathic Tendencies."

- Inside the Fight for Affordable Housing: Avery Headley Joins Terran Lamp for a Candid Bronx Leadership Conversation

- Canterbury Hotel Group Announces the Opening of the TownePlace Suites by Marriott Portland Airport

Deposit accounts, totaling $487.5 million on September 30, 2025, declined by $851,000 since the beginning of the fiscal year. Growth in local deposits during the first fiscal quarter has allowed the Bank to retire $17.2 million of higher-costing wholesale funding. Conversely, local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.56% for the current quarter compared to 2.71% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.70% for the quarter, compared to 2.89% for the quarter ended September 30, 2024.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At September 30, 2025, First Federal Savings Bank maintained lines of credit totaling $15.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($12.6 million) and the Federal Home Loan Bank ($82.4 million).

Stockholders' equity totaled $35.7 million on September 30, 2025, which includes a $7.8 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized if a security is sold. The increase in stockholders' equity is primarily due to the Company's earnings and a decrease in the unrealized loss on the Bank's available for sale investment portfolio. Based on the 1,704,992 outstanding common shares on September 30, 2025, the book value per share of FBPI stock was $20.93, compared to $20.63 on September 30, 2024.

On September 30, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios were 8.92%, 12.79%, and 14.01%, respectively - improvements from 8.36%, 11.76% and 12.98% on September 30, 2024.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

More on TelAve News

- Heritage at South Brunswick's Resort-Style Amenities for Any Age and Every Lifestyle

- T-TECH Partners with Japan USA Precision Tools for 2026 US Market Development of the New T-TECH 5-Axis QUICK MILL™

- Record Revenues, Debt-Free Momentum & Shareholder Dividend Ignite Investor Attention Ahead of 2026–2027 Growth Targets: IQSTEL (N A S D A Q: IQST)

- New YouTube Channel Pair Launches to Bring Entertainment Nostalgia Back to Life

- BRAG Hosts Holiday Benefit — Awards 10 Student Scholarships & Honors Timberland with the Corporate Impact Award

Source: First Bancorp of Indiana Inc

0 Comments

Latest on TelAve News

- America's Most Festive Garages Wanted for Garage.com's 2025 Holiday Contest

- FDA Accepts ANDA for KETAFREE™ as Analyst Sets $34 Price Target for NRx Pharmaceuticals: (N A S D A Q : NRXP) NRx is Poised for a massive Breakthrough

- BEC Technologies Expands MX-220 5G Industrial Router Series for Edge Connectivity

- "Latino Leaders Speak: Personal Stories of Struggle and Triumph, Volume II" Documents the Truth About Latino Excellence and Impact on American Society

- Broadway Smile Boutique Unveils Modern Website for Enhanced Patient Experience

- Oklahoma and Starlink Local Installers getting it done!

- Fenix Consulting Group Expands Orange County Office to Meet Growing Client Demand

- Signature Smiles Dental Group Unveils New User-Friendly Website

- CCHR: New Data Shows Millions of U.S. Children Caught in Escalating Psychiatric Polypharmacy

- QwickContractReview.com Launches $19 Contract Review Service to Protect Consumers from Hidden Contract Risks

- 100% Bonus Depreciation Places New Spotlight on Off The Hook Yacht Sales Inc. (N Y S E: OTH) as a Major Player in the $57 Billion U.S. Marine Market

- CNCPW Benchmarks Global Industry Standards: Integrating SEC Compliance with 3 Million TPS Architecture for Institutional Infrastructure

- The Patina Collective & Artist Jesse Draxler Debut "The Machine of Loving Grace"

- Smile! Dental Center Named 2025 "Best Dentist" in North Pittsburgh, Celebrating High-Tech Care and Heartfelt Service

- Dr. Johnny Shanks, As Seen on TV, Announces 20% Off Dental Implant Treatments | Tennessee's Leading All-on-X Provider

- Star Sleep & Wellness Expands to Pearland, Texas — Bringing Life-Changing Sleep Care to More Communities

- Fort Lauderdale Dentist Dr. Taskonak & IN A DAY SMILE Receive Emmy Nomination for Life-Changing Documentary "The Weight of a Smile"

- Men's Health Network Highlights Major 2025 Achievements & Launches New Donation Platform For Greater Impact

- BET and Soul Train Awards - GONE! - Introducing The World Hip Hop Awards

- Australian Aboriginal Cultural Immersions and First Nations Workshops